The steel industry is undergoing a significant transformation, prioritizing decarbonization to meet the increasing demand for renewable energy and electric vehicles. Innovations such as green steel and steel recycling are crucial in reducing carbon emissions as the world makes progress towards its 2050 net-zero targets.

Current State of the Global Steel Market

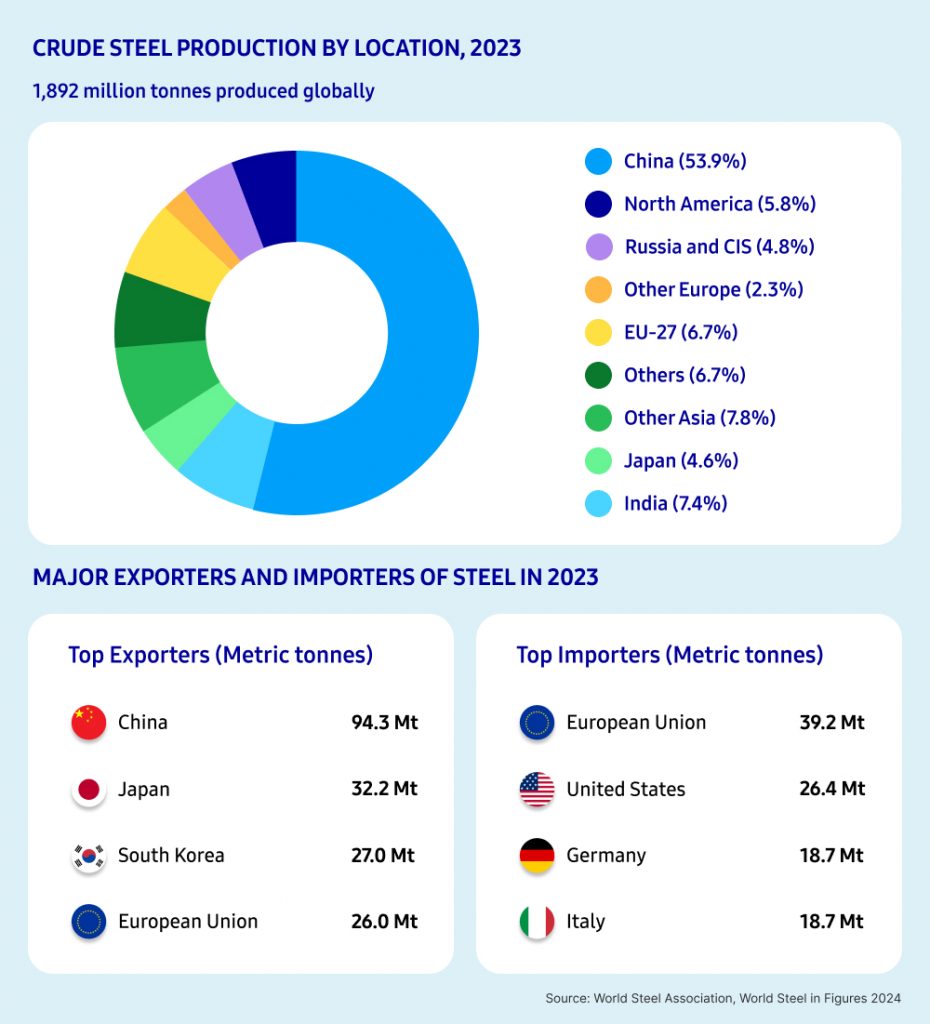

Steel is a vital material that has built the modern world as we know it. It will continue to play a vital role in creating the buildings we live in, the products we use, the machines that make our food, and the cars we drive. The global steel market is rebounding from the pandemic and geopolitical tensions, with a projected growth rate of 1.2% in steel demand by 2025, according to the World Steel Association (WSA).

In 2024, the global economy is expected to experience continued monetary tightening to stabilize inflation, with uncertainties surrounding China’s economic recovery limiting investment recovery in major countries, aside from some emerging markets like India and ASEAN. Japan and China, South Korea’s largest export markets, are expected to continue facing domestic slowdowns. In contrast, the WSA forecasts a 5% increase in steel demand in the EU, driven by inventory depletion and base effects. Within South Korea’s steel industry, solid demand from shipbuilding contrasts with uncertainties in the real estate market and a downturn in the automotive sector, suggesting limited growth potential. Consequently, major steel companies in South Korea are expected to prioritize investments in process efficiency and the development of eco-friendly products over expanding existing production capacities.

Shifting Demand and Market Dynamics

As the world shifts its focus to low-carbon energy solutions and decarbonization efforts in line with the goals of the Paris Agreement, steel demand is continuing to increase. The renewable energy sector, particularly wind and solar power, is driving the demand for steel, as is the automotive industry with the global shift to the adoption of electric vehicles (EVs). There is also an overall trend toward decarbonization in the steel industry as companies take steps toward a Net Zero future to maintain long-term competitiveness with innovations, including artificial intelligence and green steel.

However, the global steel trade is becoming increasingly competitive due to sluggish domestic demand in China and capacity expansions in ASEAN and India, leading to an oversupply in the market. This situation is exacerbated by the implementation of protectionist policies aimed at enhancing carbon competitiveness, further underscoring the urgency for steel companies to transition to environmentally sustainable production processes.

As the industry navigates these challenges, the emphasis on decarbonization will not only enhance competitiveness but also ensure long-term viability in a rapidly changing economic landscape.

Decarbonizing Steel

According to the International Energy Agency (IEA), the iron and steel sectors are the biggest CO2 emitters in the heavy industries sector. Taking steps to reduce carbon emissions in the steel sector and transforming the way steel is manufactured will be crucial for reaching net-zero targets by 2050. The IEA states that the steel industry must reduce its carbon emissions by 60% by 2050, meaning 0.6 metric tons of CO2 per metric ton of crude steel compared to today’s levels of 1.4 metric tons of CO2 per metric ton of crude steel.

The steel industry currently uses coal-dependent processes to produce steel from iron ore using integrated blast furnaces. The combustion of coal during steel manufacturing is what emits high levels of greenhouse gas emissions. The following list outlines potential pathways for steel decarbonization:

- – Green Steel

Green steel is steel that is manufactured without the use of fossil fuels and includes energy sources such as hydrogen, carbon capture, and biomass. This innovative method significantly reduces carbon emissions compared to traditional steel manufacturing processes, which heavily rely on coal and natural gas. The development of green steel is essential for reducing the environmental impact of the steel industry, which is a major contributor to global greenhouse gas emissions. - – Increasing Steel Recycling for Scrap Production

In the steel industry, increasing the use of scrap steel will help reduce CO2 emissions overall. According to the WSA, each metric ton of scrap used for steel production avoids 1.5 metric tons of carbon dioxide emissions, and the consumption of 1.4 metric tons of iron ore, 740 kg of coal, and 120 kg of limestone. Additionally, recycling steel requires significantly less energy compared to producing new steel from raw materials, resulting in further reductions in greenhouse gas emissions.

AI-Driven Advancements in the Steel Industry

Technological innovation in the global steel industry is needed to drive long-term competitiveness and increase efficiency. In recent years, companies have been implementing artificial intelligence (AI) solutions into steel manufacturing processes to reduce costs, ensure a high level of quality, increase efficiency, and produce more product volume. As the Boston Consulting Group points out, the steel industry’s long history means that steel mills may not be set up in a way that supports this technology, making the industry slow to adapt.

Market Outlook for the Steel Industry

The global steel industry was valued at an estimated $1,893.9 billion USD in 2023. This is projected to grow at a compound annual growth rate (CAGR) of 4.4% to $2,901.9 billion USD by 2033. This surge in demand reflects the steel industry’s vital role in the modern world and its continued importance over the next decade.

According to the WSA’s short-term outlook for the steel industry, India is expected to be a key market with a forecast of 8% growth in its steel demand over 2024 and 2025, driven by strong infrastructure investments. Southeast Asia and the Middle East are also expected to show accelerated steel demand growth, while demand in Europe will pick up again, and steel demand remains steady in the U.S., Japan, and South Korea. China’s steel demand is predicted to decline by 1% in 2025, remaining significantly lower than its peak in 2020.

Carbon Steel: Key Applications and Market Projections

Global carbon steel sales stood at $1.05 billion USD in 2023 and is projected to have a year-on-year growth of 3.6% in 2024 and reach $1.09 billion USD in 2024. Carbon steel demand is estimated to reach $1.26 billion USD by 2034, with a CAGR of 4% over the next ten years.

Stainless Steel: Key Applications and Market Projections

In 2023, the global stainless steel market was valued at $126.38 billion USD. It is projected to reach $215.89 billion USD by the year 2033, with a CAGR of 3.1%. Due to the strength, flexibility, recyclability, and corrosion-resistance of stainless steel, industry experts predict steady growth and demand for stainless steel in the future for big industries, household appliances, and electronics.

Samsung C&T Trading and Investment Global Steel Trading Network

Samsung C&T Trading and Investment Group has over 50 years of expertise in steel trading and an extensive global network. The Group conducts global trading of industrial steel products, including crude steel, flat products, and stainless steel, serving clients in the automotive, electronics, and construction industries. Samsung C&T T&I Group operates coil centers and precision stainless steel plants, enhancing the value chain from processing to distribution, while providing top-notch service to our customers.

As a global leader in the steel trading industry, the Group is committed to exceptional customer service and supplying high-quality steel products in collaboration with major global steelmakers.